Context

- Recently, the Reserve Bank of India (RBI) issued a draft review of the “Scale Based Regulation” (SBR) to streamline the identification of Upper Layer NBFCs (NBFC-UL). The RBI proposes to replace the current complex scoring methodology with a transparent, absolute asset-size threshold of ₹1,00,000 crore.

- This change aims to provide regulatory clarity for large entities, including Core Investment Companies (CICs) and government-owned lenders, regarding their mandatory listing and enhanced capital requirements.

What is an NBFC?

A Non-Banking Financial Company (NBFC) is a financial institution registered under the Companies Act, 1956/2013, that provides banking services without meeting the legal definition of a bank.

- Principal Business: A company is classified as an NBFC if its financial assets constitute more than 50% of its total assets, and its income from financial assets constitutes more than 50% of its gross income (the 50-50 test).

- Key Distinctions from Banks:

- NBFCs cannot accept demand deposits (savings or current accounts).

- They do not form part of the Payment and Settlement System; hence, they cannot issue cheques drawn on themselves.

- The Deposit Insurance and Credit Guarantee Corporation (DICGC) facility is not available to NBFC depositors.

- Regulation: Primarily regulated by the RBI under the RBI Act, 1934. However, certain NBFCs like Insurance companies (IRDAI), Stock Broking (SEBI), and Nidhi companies (MCA) are regulated by other bodies.

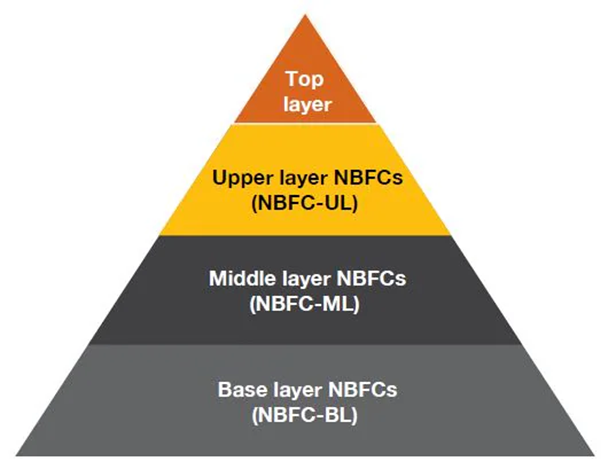

The Scale-Based Regulation (SBR) Framework

The SBR framework (effective since 2022) organizes NBFCs into four layers based on their size, activity, and risk.

| Layer | Criteria & Composition |

| Base Layer (NBFC-BL) | Non-deposit taking NBFCs with assets < ₹1,000 crore; includes P2P platforms and Account Aggregators. |

| Middle Layer (NBFC-ML) | All deposit-taking NBFCs (regardless of size); Non-deposit NBFCs with assets ≥ ₹1,000 crore; HFCs and SPDs. |

| Upper Layer (NBFC-UL) | Identified by RBI as “systemically significant.” Requires higher capital (CET-1) and mandatory listing. |

| Top Layer (NBFC-TL) | Remains empty by default; populated only if the RBI finds a specific NBFC-UL poses extreme systemic risk. |

Key Proposed Changes in the RBI Review

- Simplified Threshold: Instead of the current “top 10” rule and parametric scoring, any NBFC with assets of ₹1 lakh crore and above will automatically enter the Upper Layer.

- Inclusion of PSUs: Government-owned NBFCs (like PFC and REC) will no longer be restricted to the Middle Layer. If they meet the asset size, they will face the same stringent regulations as private NBFC-ULs.

- Credit Risk Transfers: NBFC-ULs can now use State Government Guarantees as risk mitigants without a cap, attracting a lower risk weight of 20%, aligning them with bank-like standards.

- Mandatory Listing: Entities identified as NBFC-UL are required to list on a stock exchange within three years. The new asset-based rule reinforces this requirement for large conglomerates and core investment companies (CICs) that exceed the ₹1 lakh crore mark

Q. With reference to the Non-Banking Financial Companies (NBFCs) in India, consider the following statements:

1. An NBFC cannot accept demand deposits from the public.

2. Under the Scale-Based Regulation (SBR), all Housing Finance Companies (HFCs) are classified in the Base Layer.

3. The RBI has proposed an absolute asset-size threshold of ₹1 lakh crore for an NBFC to be classified in the Upper Layer.

Which of the statements given above are correct?

A) 1 and 2 only

B) 2 and 3 only

C) 1 and 3 only

D) 1, 2, and 3

Answer: C) 1 and 3 only

Solution:

• STATEMENT 1 IS CORRECT: NBFCs are legally barred from accepting demand deposits (savings/current accounts); they can only accept term deposits if specifically authorized.

• STATEMENT 2 IS INCORRECT: Under the SBR framework, all Housing Finance Companies (HFCs) are placed in the Middle Layer (NBFC-ML), not the Base Layer.

• STATEMENT 3 IS CORRECT: The 2026 RBI draft review proposes a transparent threshold of ₹1,00,000 crore (₹1 lakh crore) for identification in the Upper Layer.